Lifetime allowance (LTA)

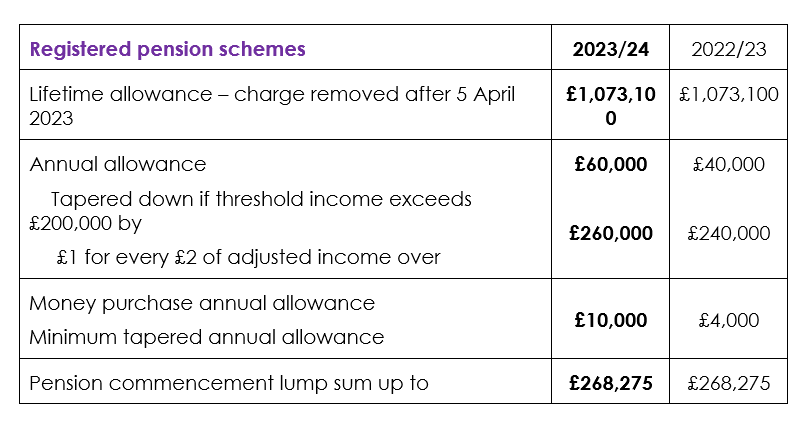

The Chancellor announced the abolition of the LTA. The 55% and 25% LTA charge tax rates that apply when an individual exceeds the LTA for pension savings will be reduced to nil from 6 April 2023. Consequently, nobody will face an LTA tax charge from that date.

At an unspecified future date, the government will entirely remove the LTA from pensions tax legislation.

Annual allowance (AA)

For 2023/24, the AA for pension contributions will increase to £60,000. The AA is subject to tapering when an individual’s threshold income exceeds £200,000 and their adjusted income exceeds £260,000. The minimum AA resulting from the application of the taper rules will be increased from £4,000 to £10,000 (applying when adjusted income is £360,000 or more).

The money purchase annual allowance (MPAA), applying to those who have drawn pension benefits flexibly, will also rise from £4,000 to £10,000.

Pension commencement lump sum (PCLS) – upper monetary cap

The maximum tax-free PCLS of up to 25% of a pension fund will remain frozen. From 2023/24, there will be a new monetary limit on the total PCLS of £268,275 (equivalent to 25% of the current standard LTA). If a lump sum is drawn above this level, the excess will be subject to income tax.

Pensions relief relating to net pay arrangements

From 2024/25, legislation will make top-up payments to individuals who have a total income below the personal allowance and save into a pension scheme using a net pay arrangement. The measure will take effect from 6 April 2025, with the top-up payments made as soon as possible after the tax year in which the contribution is paid.

SAVER ACTION POINT

Investing in pensions. You may be able to make much larger pension contributions in 2023/24 as the annual allowance has gone up to a maximum of £60,000.

Individual savings account (ISA) subscription limits

The ISA annual subscription limit for 2023/24 will remain at £20,000 and the corresponding limit for junior ISAs (JISAs) and child trust funds (CTFs) will stay at £9,000.

Always seek expert financial advice.